We are pleased to share that our operations have been reorganised across new premises to better support our clients and growing team. Our offices will be located at the following addresses:

Singapore's Budget 2025 introduces targeted tax and incentive measures to support businesses amid evolving global challenges. Here are some highlights of the key changes and how they may impact your business.

Corporate Income Tax Rebate & Cash Grant

To help businesses manage operating costs and maintain competitiveness, the government has introduced a Corporate Income Tax (CIT) Rebate and Cash Grant scheme for Year of Assessment (YA) 2025:

50% CIT Rebate will be automatically granted to all companies based on their tax payable.

Minimum $2,000 Cash Grant for companies that:

Were active in Calendar Year (CY) 2024, and

Employed at least one local employee in the same year.

The maximum combined benefit from the rebate and cash grant is capped at $40,000 per company.

Eligible companies will automatically receive the payout from the second quarter of 2025 onwards.

The PWCS continues to support employers in uplifting lower-wage workers, with enhanced co-funding levels announced for the next two years:

For wage increases in 2025:

Government co-funding raised from 30% to 40%

Payout to be made in Q1 2026

For wage increases in 2026:

Government co-funding raised from 15% to 20%

Payout to be made in Q1 2027

This transitional wage support helps businesses adapt to rising wages while staying competitive.

🧾 Tax Rebates at a Glance

Corporate Tax Rebate: 50% rebate on corporate income tax for YA 2025, minimum $2,000 benefit, capped at $40,000.

Personal Tax Rebate: Individuals will receive a 60% income tax rebate for YA 2025, capped at $200 per taxpayer.

International Expansion & Financing Support

Market Readiness Assistance (MRA) Grant: Extended until 31 March 2026, this grant offers up to S$100,000 per new market to support SMEs in overseas market promotion, business development, and setup costs.

Double Tax Deduction for Internationalisation (DTDi): Extended until 31 December 2030, allowing businesses to claim a 200% tax deduction on qualifying expenses for international market expansion and investment development.

Enterprise Financing Scheme (EFS):

Trade Loan: The maximum loan quantum is permanently increased from S$5 million to S$10 million to support businesses' trade financing needs.

Mergers & Acquisitions (M&A) Loan: From 1 April 2025 to 31 March 2030, the scope is expanded to include targeted asset acquisitions, providing more flexible financing options for businesses pursuing growth through acquisitions.

💻 Digital Transformation & Innovation

Enterprise Compute Initiative: A new program allocating up to S$150 million to assist businesses in integrating artificial intelligence (AI) solutions through partnerships with major cloud service providers, enhancing digital capabilities and competitiveness.

SkillsFuture Workforce Development Grant: Introduced to provide up to 70% funding for job redesign activities, helping businesses adapt to technological advancements and evolving job roles.

Revamped SkillsFuture Enterprise Credit: Launching in the second half of 2026, this redesigned credit offers S$10,000 per company in an online wallet format, simplifying the process of offsetting costs for workforce and enterprise transformation initiatives.

🧓 Inclusive Employment Support

Senior Employment Credit (SEC): Extended until 31 December 2026, this scheme provides wage offsets of up to 7% for employers hiring Singaporean workers aged 60 and above earning up to S$4,000 per month, encouraging the employment of senior workers.

Uplifting Employment Credit: Extended to end-2028, this initiative offers wage offsets to employers hiring ex-offenders, promoting inclusive hiring practices and expanding the talent pool for businesses.

Budget 2022 Overview

Support for Workers and Businesses

Progressive Wage Credit Scheme (PWCS)

The Progressive Wage Credit Scheme (PWCS) provides transitional wage support for employers to adjust to upcoming mandatory wage increases for lower-wage workers covered by the Progressive Wage and Local Qualifying Salary requirements and voluntarily raise wages of lower-wage workers.

The PWCS will have the following design:

Singapore Citizen and Permanent Resident employees are eligible

Support for wage increases up to $2,500 gross monthly wage ceiling will run from 2022 to 2026

Support for wage increases above $2,500 gross monthly wage and up to $3,000 ceiling will run from 2022 to 2024.

Average gross monthly wage increase must be at least $100 in each qualifying year to be eligible for PWCS.

Eligible wage increases in each qualifying year will be co-funded for two years.

The Government will co-fund wage increases of eligible resident employees from 2022 to 2026. IRAS will notify eligible employers and they can expect to receive the first payout by the 1st Quarter of 2023.

Small Business Recovery Grant (SBRG)

The Small Business Recovery Grant (SBRG) provides one-off cash for SMEs that have been most affected by COVID-19 restrictions over the past year, like those in the F&B, Retail, Tourism and Hospitality sectors.

Eligible firms will receive S$1,000 for each local employee with mandatory CPF contributions in the period from 1 November 2021 to 31 December 20213, up to a cap of S$10,000 per firm.

Sole proprietorships and partnerships that are run by at least one local business owner4 but do not hire any local employees will receive a flat payout of S$1,000, if the local business owner is earning a net trade income of no more than S$100,000 filed with IRAS in the Year of Assessment 2021 by 31 December 2021.

IRAS will notify eligible firms starting from June 2022.

Jobs Growth Incentive (JGI)

The Jobs Growth Incentive will be extended by six months to September 2022, with stepped-down rates reflecting the improved labour market conditions.

This extension will only cover mature workers aged 40 and above who have not been employed for six months or more, persons with disabilities, and ex-offenders.

Employers do NOT need to apply for the JGI. IRAS will notify eligible employers by post of the amount of JGI payout payable to them.

They can also log in to myTax Portal to view the electronic copy of their letter.

Tax Changes on Individuals

Enhance the progressivity of Personal Income Tax (“PIT”) of tax-resident individual taxpayers

To achieve greater progressivity, the top marginal personal income tax rate will be increased with effect from YA 2024.

Chargeable income in excess of $500,000 up to $1 million will be taxed at 23%, while that in excess of $1 million will be taxed at 24%; both up from the current rate of 22%

The PIT rates for non-tax-resident individual taxpayers (except on employment income and certain income taxable at reduced withholding tax rates) will correspondingly be raised from 22% to 24%

Extend the WHT exemption for non-tax-resident mediators

The existing WHT tax exemption, introduced in 2015, has supported Singapore’s development as an international mediation hub. To build on the momentum, the Government will continue to support the international mediation sector through a holistic suite of policies and initiatives.

The WHT tax exemption will be extended till 31 March 2023.

From 1 April 2023 to 31 Dec 2027, gross income derived by non-tax-resident mediators from mediation work carried out in Singapore will be subject to a concessionary WHT tax rate of 10%, subject to conditions. Alternatively, non-resident mediators may elect to be taxed at 24% on the net income, instead of 10% on gross income.

Extend the WHT exemption for non-tax-resident arbitrators

The existing WHT tax exemption, introduced in 2002, has supported Singapore’s development as an international arbitration hub. To build on the momentum, the Government will continue to support the international arbitration sector through a holistic suite of policies and initiatives.

The WHT tax exemption will be extended till 31 March 2023.

From 1 April 2023 to 31 Dec 2027, gross income derived by non-tax-resident arbitrators from arbitration work carried out in Singapore will be subject to a concessionary WHT tax rate of 10%, subject to conditions. Alternatively, non-tax resident arbitrators may elect to be taxed at 24% on the net income, instead of 10% on gross income.

Tax Changes on Goods and Services Tax (GST)

Increase the GST rate to meet increased recurrent spending needs.

The GST rate will be increased in two steps:

a) From 7% to 8% with effect from 1 January 2023; and

b) From 8% to 9% with effect from 1 January 2024.

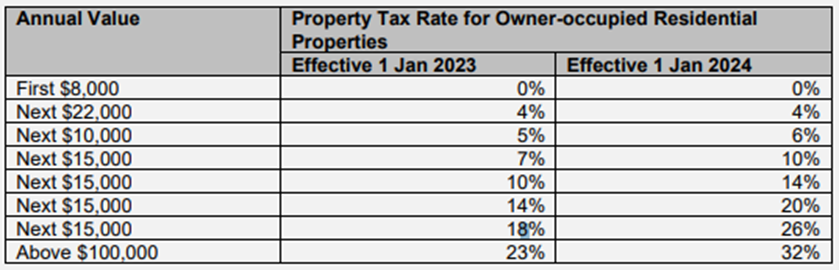

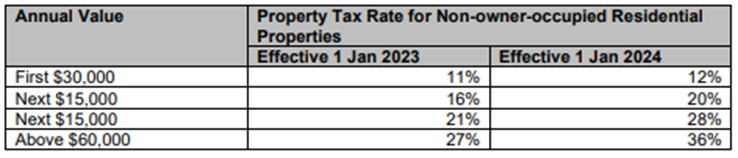

Tax Changes on Property Tax

Owner-occupied residential properties

The progressive property tax rates for owner-occupied residential properties will be revised for the portion of annual value in excess of $30,000. This change will be phased in over two years as shown below:

Non-owner-occupied residential properties

The progressive property tax rates for non-owner-occupied residential properties will be revised. This change will be phased in over two years as shown below:

Some Highlights Of Budget 2021

Supporting For Business

Jobs Support Scheme (JSS)

Extend support for

Tier 1 sectors (Eg. Aviation, Aerospace, and tourism)

30% for wages paid from Apr to Jun 2021, and 10% for wages paid from Jul to Sept 2021

Tier 2 sectors (Eg. Retail, Arts and Culture, Food Services, and Build Environment)

10% for wages paid from Apr to Jun 2021

Continue support for firms in some other sectors till Mar 2021

Further Support for Specific Sectors

Aviation - Extend cost relief

Land transport - Driver Relief fund for taxi and private hire car drivers

Arts & Culture and Sports - Resilience Packages

Jobs Growth Incentive’s (JGI)

Extend JGI qualifying window to end of Sep 2021 and eligible for companies that hire locals between Mar 2021 to Sep 2021.

For non-mature locals

Up to 12 months based on 25% of the first $5,000 of gross monthly income, from the month of hire

For mature workers (aged 40 and above), persons with disabilities and ex-offenders

Up to 18 months based on 50% of the first $6,000 of gross monthly income

Eligible companies that had hired locals between Sep 2020 and Feb 2021 will enjoy enhanced support from Mar 2021

Wage Credit Scheme (WCS)

Extended by 1 year to 2021. Government co-funding ratio at 15% and the qualifying gross wage ceiling at $5,000

High-Growth Enterprises

Extend and Enhance Financing Scheme – Venture Debt Programme

Increase cap on loan quantum from $5 million to $8 million

Mature Enterprises: Micro, SMEs and Large Enterprises

New Emerging Technology Programme

CTO-as-a-Service: access to professional IT consultancies

Digital Leaders Programme

Extend Enhanced Support Schemes to up to 80% to end of Mar 2022

Large Local Enterprises

Local Enterprises Funding platform to support enterprises scale up and expand overseas

Tax Changes

Extension of scheme/ support:

Enhancement to the carry-back relief scheme for YA 2020 will be extended to apply to qualifying deductions for YA 2021

Option to accelerate the write-off of the cost of acquiring Plant and Machinery (“P&M”) will be extended to capital expenditure incurred in the basis period for YA 2022 (ie FY 2021)

Option to claim Renovation and Refurbishment (“R&R”) deduction will be extended to qualifying expenditure incurred in the basis period for YA 2022 (ie FY 2021)

Business and IPC Partnership Scheme (“BIPS”) will be extended to 31 Dec 2023

Not-for-Profit Organisation (“NPO”) tax incentive will be extended to 31 Dec 2027

250% Tax Reduction for Qualifying Donations will be extended to 31 Dec 2023

Other changes:

Double Tax Deduction for Internationalism scheme

Automation Support Package will lapse after 31 Mar 2021

Enterprise Development Grant and Enterprise Financing Scheme continue to be available to support automation, productivity and scale-up efforts

100% Investment Allowance (“IA”) to support automation will be extended 2 years, for automation projects approved by Enterprise Singapore from 1 Apr 2021 to 31 Mar 2023

Changes of GST

Effective from 1 Jan 2023, GST will be extended to

Low-value goods which are imported via air or post

Business-to-consumer imported on non-digital services

Change of basis for determining whether zero-rating applies to a supply of media sales, from the place of circulation of the advertisement to the customer and direct beneficiary of the service belong

Covid-19 Impact on Financial Reporting

Covid-19 pandemic has affected the global economies and most of the entities, directly or indirectly, which in turn has significant implications on financial reporting.

This article highlights the impact of Covid-19 on financial reporting and provide a summary of key considerations to focus on the financial statement.

Basis of Preparation of Financial Statements

1. Assessment of Going Concern

Due to the pandemic, business entities are expected to deal with many uncertainties. The assessment on the entity’s ability to continue as a going concern basis need to be disclosed in the financial statements.

The disclosure should include

significant assumptions and judgements applied

conditions and events that raise the substantial doubt on the entity’s ability to continue as a going concern

entity’s plan to address the challenges and the progress made

If the entity has no real alternatives, but to liquidate or cease the business, it is no longer a going concern and the financial statements should have to prepared in other basis, such as “liquidation”.

The impact of Covid-19 on entities will change, but the uncertainties will remain for most of the entities.

Entities required to consider which events after the reporting date might be adjusting events and disclose the material non-adjusting event (nature of event and estimate of its financial effect).

Adjusting event

Non-adjusting event

Provide evidence of conditions that existed at the end of the reporting period

Indicative of conditions that arise after the end of reporting period

Reflected in adjustment to financial statement

Do not reflected in adjustment to financial statements, but disclosure required if material Example: decline in fair value of investments, changes of asset, breaches of loan covenants, management restructuring plan, new government reliefs

Key Considerations on Financial Statement Areas

1. Impairment of non-financial assets

Economic disruption that caused by the pandemic may trigger the need for impairment testing. The disclosure is important to understand the degree of estimation uncertainty about the recoverable amount and sensitivity of the recoverable amount to possible changes.

Management may consider:

Determine CGUs performance and changes of consumption patterns

Cash flow projections adjusted to reflect the impact of Covid-19 (impact due to trade restriction, government shutdowns, change of growth rates, etc)

Discount rates applied in recent valuations been updated to reflect the risk environment

Disclose key assumption and major sources of estimation made by management on recoverable amounts

2. Fair value measurement

The fair value of an asset (or liability) should reflect market conditions at the measurement date.

Management may consider:

Assumption of market participants based on the market condition reflected in valuation

Include risk premiums due to the impact of Covid-19 (such as credit risk and liquidity risk, forecasting risk, foreign exchange risk and commodity price risk)

Disclose significant increases of unobservable inputs that result in a Level 3 categorisation

Disclose further key assumption and major sources of estimation made by management on valuation

3. Recoverability of deferred tax assets

The projection of future taxable profits that used to assess the recoverability of deferred tax assets may affected due to the changes of forecast cash flows, changes of company’s tax strategies and government measures in response to the pandemic.

Changes of company’s plan to repatriate or distribute profits of a subsidiary that will result the recognition of a deferred tax liability

Disclose key assumption and major sources of estimation made by management in recognising and measuring deferred tax assets

4. Recoverability of revenue-cycle assets

The Covid-19 has caused adverse impact on many company’s revenue cycles due to the decrease of customer demand, customer bad debt, trade restriction, etc.

Management may consider:

Assess both contract assets and receivables for impairment (ie using an expected credit loss model)

Estimated net realisable value for inventory adjusted based on the changes in customer demand and increase of labour cost (ie estimated selling prices and estimated costs to complete)

Capitalised contract costs, to consider the changes of expected customer renewals or expected timing for completion of project

Disclose key assumption and major sources of estimation made by management in measuring revenue related assets

5. Capitalisation of borrowing costs

There might be suspension of project due to trade restriction or disruption. Thereafter, the adjustment of interest expenses for renegotiation or modification of borrowing terms may affect the amount of eligible borrowings costs.

Management may consider:

Whether the interruption is for only short term or due to common external event

Ensure the amount to be capitalised if borrowing costs continue to be capitalised

6. Other areas

If there is no change of shares proportions, de-consolidation of subsidiary is allowed only when there was a loss of control over the subsidiary

If there is loan or financial instruments pegged to InterBank Offered Rates will be converted to an alternate benchmark and hedging done on the interest rate risk, to consider Phase 1 amendments to financial instruments standard and seek professional advice.

New requirements to lodge information on Singapore's register of registrable controllers

In addition with the existing requirement to maintain the Registers of Registrable Controllers (“RORC”) at registered office, Accounting and Corporate Regulatory Authority (“ACRA”) has an additional requirement for all companies, foreign companies and Limited Liability Partnerships (“LLP”), unless exempted, to lodge information on the register with ACRA via BizFile+ in July 2020. ACRA will provide Registered Filing Agents with a further notification when the transaction in Bizfile is available for lodgement.

The RORC information lodged with ACRA will be accessible to public agencies in Singapore such as law enforcement agencies. Members of the public will not be able to access the RORC information or purchase any extracts of these lodgements.

Failing to lodge RORC with ACRA when the law takes effect shall be liable upon conviction, to a fine not exceeding $5,000.

What is Cloud Accounting

Cloud accounting is accounting using software accessed over the internet that is hosted remotely on the cloud. All functions are performed off-site and users access the applications remotely through the internet.

Why cloud accounting?

Nothing to install. Access financial data in one place online. Free and instantly updates.

Real-time insights. Capture, track, and manage accounts with ease and easily.

Bank feeds. Keep track of daily updates and simple reconciling transactions.

Online document storage. Financial data backed up on the cloud platform securely and automatically.

Online quotes and invoicing. Keep your cash flow healthy and get paid faster by online options.

Improved efficiency. Reduce business costs and monitor the business in a better way.

Future of cloud accounting "To stay competitive in today's streaming world, business face growing pressure to innovate faster - and the cloud is helping them keep pace." -- Research on future cloud computing from Google

FMD is supporting for cloud accounting now!!

Singapore Budget 2020

Highlight on Corporate Tax √ Tax rate remain at 17% √ Tax rebate for YA 2020 granted at 25%, subject to a cap of $15,000 √ Additional 2 months of interest-free instalment if company paying CIT by Giro and file ECI within 3 months from financial year end

During period from 19.02.2020 to 31.12.2020

Before 19.02.2020 and has ongoing instalment payments to be made in March 2020

√ Enhanced carried-back relief system

The number of YAs to which unutilised Capital Allowances (CA) and trade losses from YA 2020 can be carried back will be increased from one YA to three YAs immediately preceding YA 2020 (i.e. YA 2017, YA 2018 and YA 2019).

Businesses may elect for the enhanced carry-back relief based on an estimate of the current year unutilised CAs and trade losses for YA 2020.

√ Plant and Machinery

Accelerate the write-off of the cost for plant and machinery acquire in financial year 2020.

Streamline the prescribed working life of P&M in the Sixth Schedule for capital allowance claims under Section 19

1. Option to write-off over 2 years

2. 75% in the first YA 2021 and 25% in the second YA 2022

3. No deferment of CA claims is allowed

√ Renovation and Refurbishment (R&R)

Accelerate the deduction of expenses for qualifying R&R incur in year 2020 with option to claim in 1 YA (subject to the cap of $300,000 for every relevant period of 3 consecutive YA)

√ Capital grants

Claim will not be allowed for tax deduction or allowances on expenditure funded by the grant from the government/statutory boards for capital grants approved on or after 1st January 2021

√ Schemes :

Double Tax Deduction for Internationalism (DRDi) scheme will be extended until 31 December 2025 with expanded scope for expenses incurred on or after 1 April 2020

Mergers & Acquisitions (M&A) Scheme will be extended until 31 December 2025

Scheme under Section 13Z will extend and refine the upfront certainty of non-taxation for companies’ gains on disposal of ordinary shares from 1 June 2022 to 31 December 2027. This is not applicable to disposal of unlisted shares in an investee company that is in the business of trading, holding or developing immovable properties in Singapore or overseas.

Land Intensification Allowance (LIA) scheme will be extended until 31 December 2025

Further tax deduction scheme for research and development (R&D) under Section 14E, incentive will lapse after 31 March 2020

Highlight on Personal Tax √ Personal tax rate remains with top line rate of 22% of chargeable income in excess of $320k

√ Non-resident mediators and arbitrators: Withholding Tax Exemption (WTH) will be extended until 31 March 2022

√ Non-resident public entertainers: 10% concessionary WTH will be lapsed after 31 March 2022

√ Angel Investors Tax Deduction (AITD) will be lapsed after 31 March 2020

Highlight on Property tax

Rebates available as per following : √ 30% for accommodation and function room of hotels and service apartments, MICE space components of prescribed MICE; √ 15% for international airport, cruise or ferry terminal and shops located in hotels and service apartments, prescribed MICE venues and premises of tourist attraction;

Useful Tax Information For Corporate in Singapore

To attract and keep global investments, Singapore has implemented a low corporate income tax rates and various tax incentives that subsequently contribute to the economic growth.

Single-tier income tax system

Singapore has adopted a single-tier corporate income tax system since year 2003. That means the tax paid by a company on its chargeable income is the final tax and dividends received by the shareholders from the company will not be subject to tax.

Basis Period for Income Tax

Year of Assessment (YA) refers to the year in which income tax is calculated and charged. In Singapore, corporate tax income is assessed in the preceding year basis. For example, if the income is earned in the financial year 2018, it will be taxed in year 2019.

Tax Structure

The corporate income tax rate has been fixed at 17% since year 2010 for both Singapore tax resident and non-Singapore tax resident companies. Tax Exemption for new start-up companies

Qualifying conditions for new start-up companies:

It must be incorporated in Singapore

It must be tax resident in Singapore for that YA

Throughout the basis period, there are 20 or less shareholders where

all of the shareholders are individuals; or

at least one individual shareholder holds at least 10% of the issued ordinary shares

The above tax exemption is however, not available to investment holding companies and properly development companies.

Corporate income tax (CIT) rebate*

Due date for tax filing

The companies in Singapore must file the income tax return by the statutory filing deadline which is 30 November every year.

Payment of Tax Liability

Notwithstanding any objection or appeal against the Notice of Assessment raised, the tax liability has to be paid within 1 month after the service of that Notice.

Objections to the Notice of Assessment raised

If the company disputes the assessment, an objection has to be made within 60 days from the date of service of the Notice of Assessment stating precisely the grounds of the objection. Otherwise, the assessment may be treated by the Comptroller as final.

Withholding Tax

Certain payment made to non-residents like interest, royalty, technical assistance, rental, directors’ fee, etc are subject to withholding tax requirements unless exempt under the double taxation agreement arrangement with various countries. Withholding tax is not applicable on dividend payment.

Budget 2019 Tax Changes And Other Tax Changes Affecting YA 2020

Changes for Individuals

Personal tax rebate of 50% of tax payable cap up to $200 for Year of assessment 2019

Grandparent Caregiver Relief in respect of a handicapped and unmarried dependent child, regardless of the child's age from YA 2020

Lapse of Not Ordinarily Resident scheme after YA 2020

Changes for Businesses

Writing Down Allowance for acquisition of Intellectual Property Rights extended till last day of the basis period for YA 2025

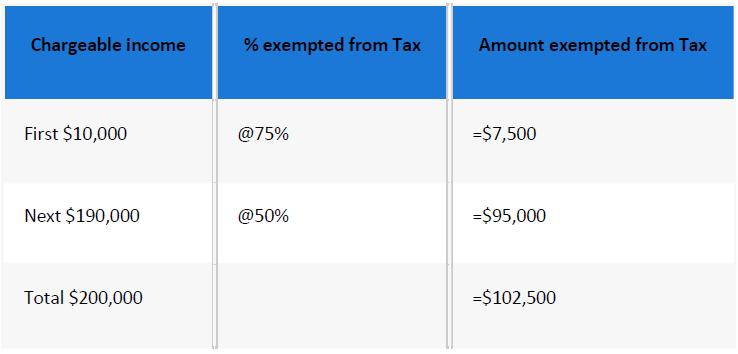

Reduced Partial tax exemption for companies (from YA 2020) Announced in previous Budget:

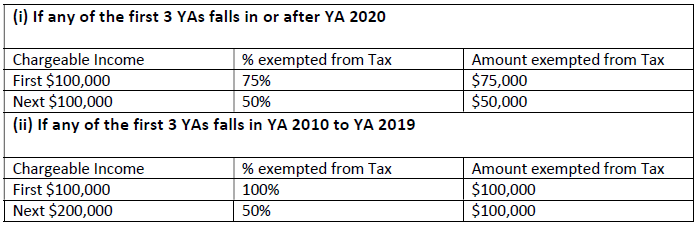

Tax exemption scheme for new start-up companies (where any of the first 3 YAs falls in or after YA 2020)