The Progressive Wage Credit Scheme (PWCS) provides transitional wage support for employers to adjust to upcoming mandatory wage increases for lower-wage workers covered by the Progressive Wage and Local Qualifying Salary requirements and voluntarily raise wages of lower-wage workers.

The PWCS will have the following design:

Singapore Citizen and Permanent Resident employees are eligible

Support for wage increases up to $2,500 gross monthly wage ceiling will run from 2022 to 2026

Support for wage increases above $2,500 gross monthly wage and up to $3,000 ceiling will run from 2022 to 2024.

Average gross monthly wage increase must be at least $100 in each qualifying year to be eligible for PWCS.

Eligible wage increases in each qualifying year will be co-funded for two years.

The Government will co-fund wage increases of eligible resident employees from 2022 to 2026. IRAS will notify eligible employers and they can expect to receive the first payout by the 1st Quarter of 2023.

Small Business Recovery Grant (SBRG)

The Small Business Recovery Grant (SBRG) provides one-off cash for SMEs that have been most affected by COVID-19 restrictions over the past year, like those in the F&B, Retail, Tourism and Hospitality sectors.

Eligible firms will receive S$1,000 for each local employee with mandatory CPF contributions in the period from 1 November 2021 to 31 December 20213, up to a cap of S$10,000 per firm.

Sole proprietorships and partnerships that are run by at least one local business owner4 but do not hire any local employees will receive a flat payout of S$1,000, if the local business owner is earning a net trade income of no more than S$100,000 filed with IRAS in the Year of Assessment 2021 by 31 December 2021.

IRAS will notify eligible firms starting from June 2022.

Jobs Growth Incentive (JGI)

The Jobs Growth Incentive will be extended by six months to September 2022, with stepped-down rates reflecting the improved labour market conditions.

This extension will only cover mature workers aged 40 and above who have not been employed for six months or more, persons with disabilities, and ex-offenders.

Employers do NOT need to apply for the JGI. IRAS will notify eligible employers by post of the amount of JGI payout payable to them.

They can also log in to myTax Portal to view the electronic copy of their letter.

Tax Changes on Individuals

Enhance the progressivity of Personal Income Tax (“PIT”) of tax-resident individual taxpayers

To achieve greater progressivity, the top marginal personal income tax rate will be increased with effect from YA 2024.

Chargeable income in excess of $500,000 up to $1 million will be taxed at 23%, while that in excess of $1 million will be taxed at 24%; both up from the current rate of 22%

The PIT rates for non-tax-resident individual taxpayers (except on employment income and certain income taxable at reduced withholding tax rates) will correspondingly be raised from 22% to 24%

Extend the WHT exemption for non-tax-resident mediators

The existing WHT tax exemption, introduced in 2015, has supported Singapore’s development as an international mediation hub. To build on the momentum, the Government will continue to support the international mediation sector through a holistic suite of policies and initiatives.

The WHT tax exemption will be extended till 31 March 2023.

From 1 April 2023 to 31 Dec 2027, gross income derived by non-tax-resident mediators from mediation work carried out in Singapore will be subject to a concessionary WHT tax rate of 10%, subject to conditions. Alternatively, non-resident mediators may elect to be taxed at 24% on the net income, instead of 10% on gross income.

Extend the WHT exemption for non-tax-resident arbitrators

The existing WHT tax exemption, introduced in 2002, has supported Singapore’s development as an international arbitration hub. To build on the momentum, the Government will continue to support the international arbitration sector through a holistic suite of policies and initiatives.

The WHT tax exemption will be extended till 31 March 2023.

From 1 April 2023 to 31 Dec 2027, gross income derived by non-tax-resident arbitrators from arbitration work carried out in Singapore will be subject to a concessionary WHT tax rate of 10%, subject to conditions. Alternatively, non-tax resident arbitrators may elect to be taxed at 24% on the net income, instead of 10% on gross income.

Tax Changes on Goods and Services Tax (GST)

Increase the GST rate to meet increased recurrent spending needs.

The GST rate will be increased in two steps:

a) From 7% to 8% with effect from 1 January 2023; and

b) From 8% to 9% with effect from 1 January 2024.

Tax Changes on Property Tax

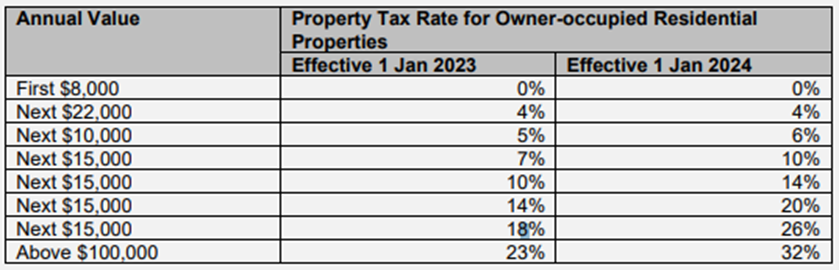

Owner-occupied residential properties

The progressive property tax rates for owner-occupied residential properties will be revised for the portion of annual value in excess of $30,000. This change will be phased in over two years as shown below:

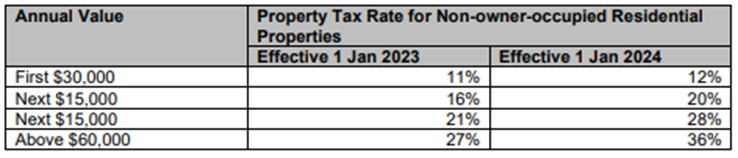

Non-owner-occupied residential properties

The progressive property tax rates for non-owner-occupied residential properties will be revised. This change will be phased in over two years as shown below: